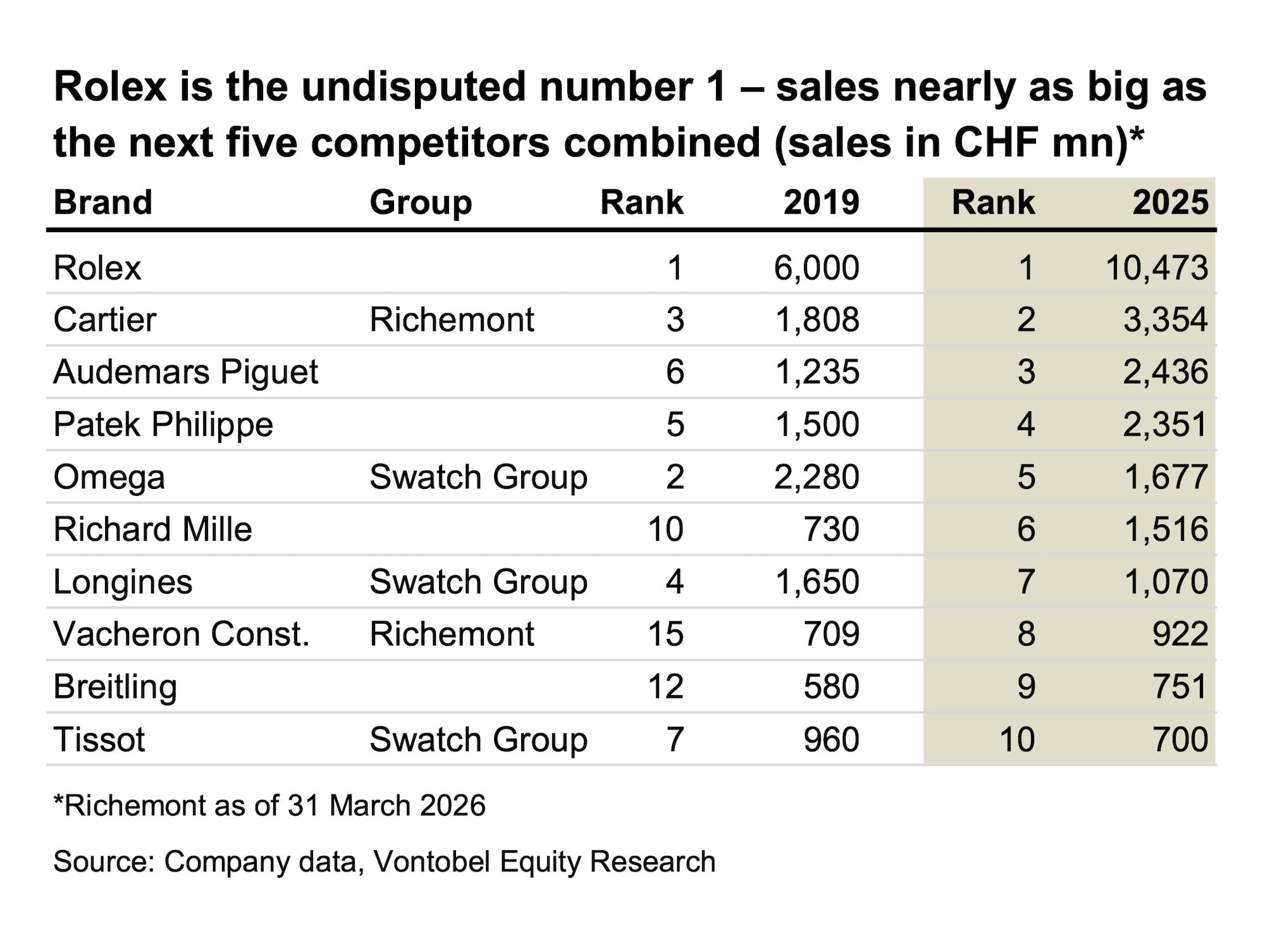

Swiss bank Vontobel is one of a handful of organisations with genuine credibility in producing an annual report on the watch industry and luxury goods more generally. Vontobel’s analysis is a must-read. Led by Jean-Philippe Bertschy, Head of Swiss Equity Research at Vontobel, the latest report provides clear indications of the current transformation of the industry. Of course, the highlight remains the following chart, ranking the top 10 watch brands in 2025, according to Vontobel’s estimates (most of these brands do not publish their financial results).

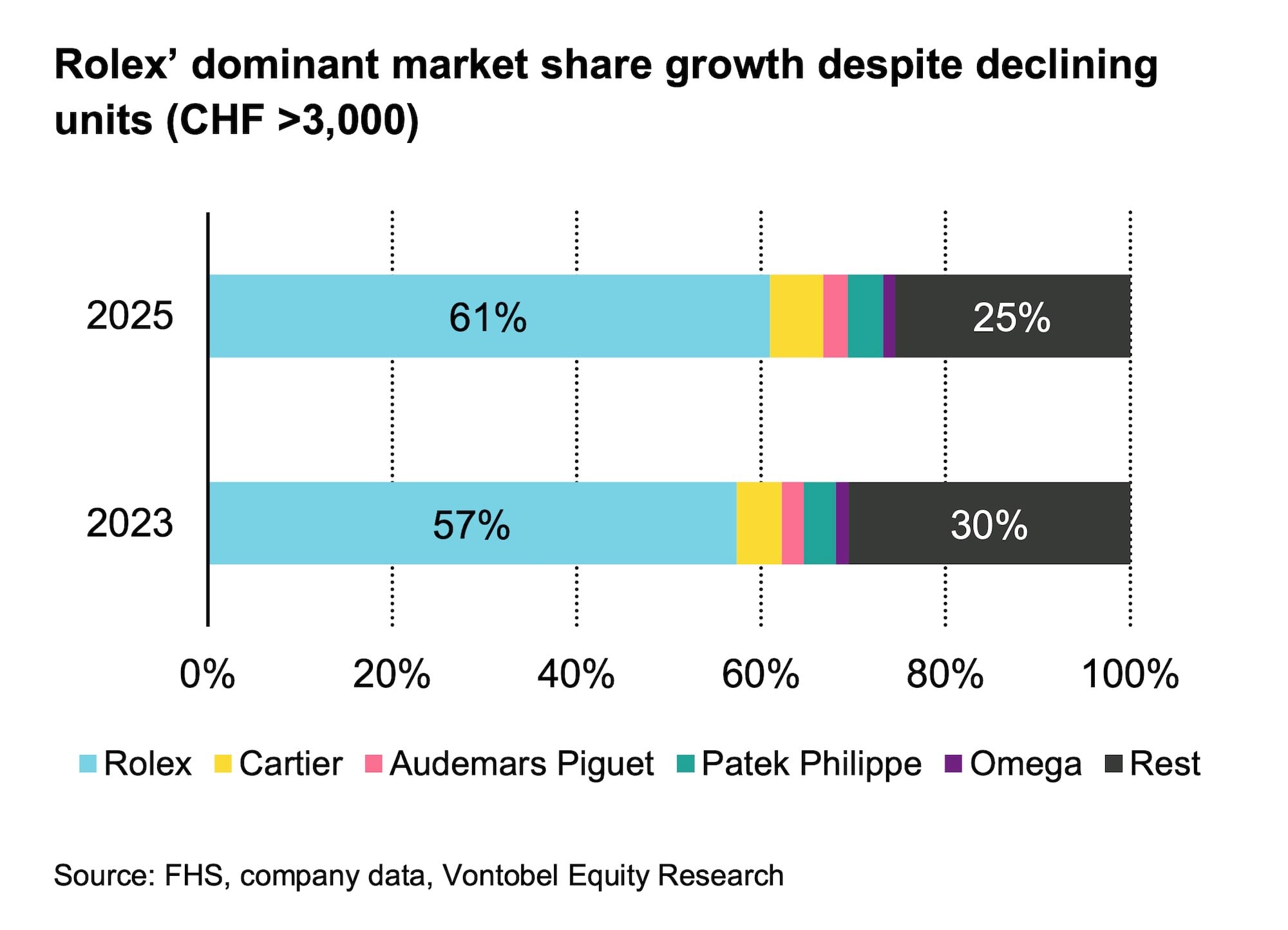

Beyond Rolex’s impressive sales, which still exceed CHF 10 billion, the most notable aspect of this chart is the relative scale of Rolex compared with its competitors. Rolex’s sales are equivalent to the combined sales of the next five competitors. This shows that there is a real polarisation of the industry, or that “the industry is becoming increasingly oligopolistic”, as Vontobel puts it. Almost all are positioned at the higher end, except Tissot and Longines, which operate in the lower segment of the industry. As the report indicates, in the “premium segment above CHF 500, the top ten brands now account for nearly 70% of export volumes, while concentration rises above 80% in the segment above CHF 3,000, underscoring the systemic importance of a handful of dominant players for the watch supply chain.” Over the past couple of years, only a handful of brands managed to maintain or grow volumes – unsurprisingly, these are large independent firms such as Patek Philippe, Audemars Piguet and Richard Mille, with Cartier also benefiting from a strong momentum.

But the situation is two-fold. While major brands report higher results, this growth masks a decline in volume in the traditional core segment of luxury Swiss-made watches (export price above CHF 3,000). As Vontobel explains, “over the past two years, the segment above CHF 3,000 has exported roughly 220,000 fewer watches, a decline of just over 10%, confirming that even the high end is not immune to volume pressure.” But that’s only one side of the coin, as in the meantime, Vontobel “estimates that watches priced above CHF 20,000 have increased substantially over the same period, by nearly 50,000 additional pieces. This implies that the “core” high-end segment between CHF 3,000 and CHF 20,000 has shrunk even more sharply.” This reinforces the idea that ultra luxury is absorbing a growing share of the industry while the core range of Swiss watches suffers, with volumes squeezed.

Last but certainly not least, Vontobel indicates that Rolex has trimmed production in 2025 for the second year in a row, but “most likely by design, as the brand prioritises scarcity and pricing power over incremental unit growth.”